A payday loan and an installment loan differ mainly in how you repay them. A payday loan requires you to repay the full amount in one lump sum, usually by your next paycheck, while an installment loan lets you repay it over time through smaller, scheduled payments. Understanding this difference helps you choose the right option for your financial situation.

Unexpected expenses happen at any time, whether it’s car repairs, medical bills, or a gap between paychecks. When you need fast financial support, you may come across two common options: a payday loan (also known as a short-term loan) and an installment loan. At first glance, they may seem similar, but they work very differently.

Choosing the right loan depends on your situation, budget, and how quickly you repay what you borrow. Some borrowers turn to a payday lender for quick access to cash, while others prefer the structure of longer-term payments.

In this guide, we’ll break down the key differences, benefits, and best use cases so you can make a confident, informed decision.

What is a payday loan?

These loans provide quick cash when you need it most; they’re typically smaller amounts meant to be repaid in full by your next paycheck.

When you work with a payday lender, the process is usually fast and straightforward. Approval often requires basic information such as proof of income and an active bank account. This makes loans accessible to many borrowers, especially those who need immediate funds.

The key feature is its repayment structure. Instead of making multiple payments over time, you repay the entire loan (including fees) in a single lump sum. Because of this, payday loans work best for short-term financial needs when you know you will repay the amount quickly.

What is an installment loan?

These loans work differently. Instead of repaying the full amount at once, you pay it back over time through a series of scheduled payments. You’ll make these payments monthly, including the loan amount and interest.

People often use these loans for larger expenses or when spreading payments over time makes more sense. This structure allows you to manage your finances more comfortably, as payments are predictable and easier to budget for.

Key differences

Understanding the differences between these two loan types helps you make the best choice:

- Repayment structure: Payday loans require a single lump-sum payment, while an installment loan gets repaid through smaller, scheduled payments

- Loan timeline: Short-term loans are exactly what they sound like: short-term. They’re often due within weeks; installments extend over months or years.

- Payment size: Short-term loans involve a single larger payment; installment loans spread repayment into manageable amounts.

- Cost and fees: Short-term loans often have higher fees because of their quick turnaround; installment loans spread costs over time.

- Flexibility: Installment loans offer greater repayment flexibility; payday loans require faster repayment.

- Approval process: A payday lender typically offers faster approvals. Installment loans may involve more review, but offer structured terms.

When a payday loan makes sense

A short-term loan can be a practical option in certain situations, especially when time is a critical factor. Consider one if you need a small amount of money quickly, have an urgent expense that can’t wait, or expect to repay the loan with your next paycheck.

Working with a trusted payday lender provides fast access to funds during a financial gap. The key is to ensure that repayment fits comfortably within your budget so you avoid additional stress.

When an installment loan is the better choice

This type of loan may be a better option when you need more flexibility and time to repay. It works well if you’re covering a larger expense, prefer predictable monthly payments, or need time to manage repayment without pressure.

Because these loans spread payments out over time, they help you plan ahead and maintain stability, which makes them a strong choice if you want a structured approach to managing your finances.

Benefits and drawbacks of each option

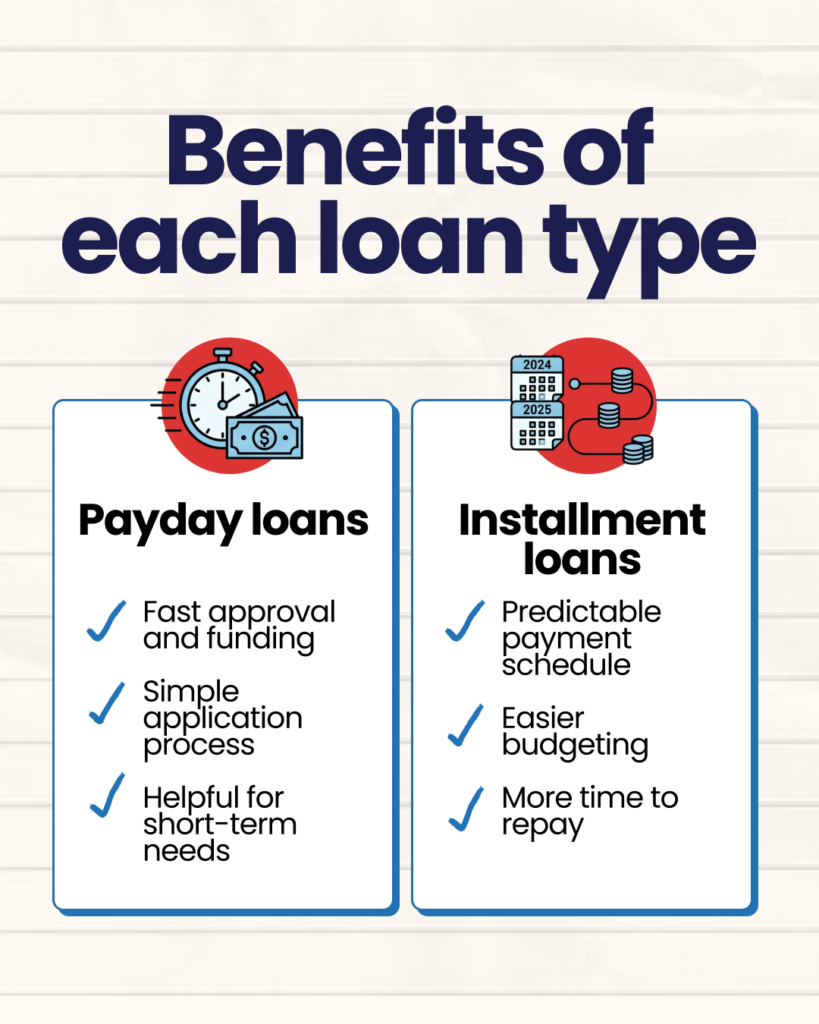

Payday loan benefits

Fast approval and funding

One of the biggest advantages is the speed with which you access funds. Many borrowers receive approval and funding within a short time, making it a helpful option when you’re facing urgent expenses that can’t wait.

Simple application process

Applying through a payday lender is typically straightforward and requires minimal documentation. Most lenders focus on basic information such as income and bank account details, which makes the process faster and more accessible than with traditional loans.

Helpful for short-term needs

Payday loans bridge temporary financial gaps, such as covering bills between paychecks or handling unexpected costs. When used responsibly, they provide quick relief without a long-term commitment.

Payday loan drawbacks

Short repayment timeline

These loans usually need to be repaid in full by your next paycheck. This short timeline puts pressure on you, especially if your budget is already tight.

Larger lump-sum payment

Because repayment happens all at once, the total amount due feels significant. This makes it important to plan ahead and ensure you’ll have the funds available on the due date.

It can be stressful if not planned properly

Without a clear repayment strategy, a short-term loan may lead to financial strain. Borrowers who don’t prepare for repayment may face additional fees or need to borrow again, creating a cycle of dependency.

Installment loan benefits

Predictable payment schedule

One of the biggest advantages is the consistency it provides. Payments are scheduled at regular intervals and remain the same throughout the loan term. This predictability makes it easier to plan ahead and avoid surprises.

Easier budgeting

Because payments are fixed and spread out over time, these loans fit more naturally into a monthly budget. Instead of preparing for one large payment, you manage smaller, steady payments alongside your regular expenses. This structure helps reduce financial strain and improves overall stability.

More time to repay

An installment loan gives you the flexibility to repay what you borrow over an extended period. This is especially helpful for larger expenses, allowing you to handle costs without putting immediate pressure on your finances. The longer timeline makes repayment feel more manageable and less overwhelming.

Installment loan drawbacks

Longer commitment

While the extended repayment period is helpful, it also means you’re committed to making payments for a longer time. This requires consistency and planning, especially if your financial situation changes during the loan term.

May involve more steps during application

Compared to a short-term loan, applying for an installment loan takes more time. Lenders may review additional information, such as credit history or financial background, before approving the loan. While this process feels slower, it often results in more structured and manageable loan terms.

Common mistakes to avoid

Choosing the right loan also means avoiding common pitfalls:

- Borrowing more than necessary: Taking out more than you need increases repayment pressure

- Not understanding the repayment terms: Always review how and when you’ll repay the loan

- Choosing speed over structure: While a short-term loan offers speed, an installment loan may offer better long-term flexibility

- Not comparing lenders: Whether you’re working with a payday lender or exploring installment options, comparing terms helps you find the best fit

- Using short-term loans repeatedly: Loans should be used as solutions, not as ongoing financial strategies

FAQ

Can you get a loan on SSDI?

Yes, you get a loan while receiving SSDI (Social Security Disability Insurance). Many lenders consider SSDI as a valid source of income. Approval depends on factors like your monthly income, expenses, and ability to repay.

What are the four types of loans?

The four common types of loans are:

- Personal loans – Flexible loans used for various expenses

- Auto loans – Used to finance a vehicle

- Mortgage loans – Used to purchase a home

- Student loans – Used to pay for education

Which loan is easier to get approved for?

A payday loan is generally easier to get approved for because the requirements are minimal. Many payday lenders focus on income rather than credit history. However, easier approval often comes with shorter repayment terms and higher fees.

Can I switch from one loan type to another?

Yes, in some cases. This is often done through refinancing or taking out a new loan to replace the old one. For example, someone might replace a short-term loan with an installment loan to gain more time to repay. Approval depends on your financial situation and the lender’s requirements.

Apply for a loan through USA Cash Services

When you’re deciding between these two loan types, the most important step is choosing a lender you trust.

At USA Cash Services, we offer both options with clear terms, fast approvals, and dependable support. Whether you need quick, short-term relief or a more structured repayment plan, our team is here to help you find the solution that fits your needs.

Take the next step with confidence. Turn to USA Cash Services for all your payday and installment loan needs and experience a straightforward, reliable approach to borrowing.