Every payday loan borrower has the right to clear, upfront information about their loan before approval. Federal and state laws require payday lenders to disclose details such as loan fees, repayment dates, and the total cost of borrowing. Understanding these rights helps consumers make informed decisions and avoid unfair or predatory lending practices.

When unexpected expenses arise, payday loans provide the fast financial help you need to get back on track. Whether it’s a medical bill, car repair, or short-term cash shortage, these loans offer quick access to funds when timing is critical.

Before signing on the dotted line, every payday loan borrower should understand their rights and what their lender is legally required to disclose.

Many borrowers don’t realize that payday lenders must follow specific federal and state regulations designed to protect consumers from confusion or high costs. These laws ensure transparency in every step of the process, so you can make an informed decision with full confidence.

Knowing what information your lender must share is empowering. Understanding your rights as a borrower helps you spot unfair practices, avoid unnecessary fees, and choose a lender you trust.

In this guide, we’ll break down the disclosures every payday lender must provide, explain why these rules exist, and show you how to use them to borrow safely, responsibly, and with complete peace of mind.

What payday lenders must disclose

Every payday lender must provide borrowers with complete, easy‑to‑understand information before approving or funding a loan.

These legally required disclosures protect consumers by ensuring that there are no hidden costs, confusing terms, or misleading promises. Transparency is at the heart of responsible lending; when you know all the details upfront, you make smarter, more confident decisions about your finances.

Here’s what every payday loan borrower should expect to receive before signing any agreement:

1. The total loan amount and fees

Your lender must clearly state how much you’ll receive and the total repayment amount by the due date. This figure includes the principal loan amount and every applicable fee. For example, if you borrow $400 with a $60 flat fee, your full repayment obligation of $460 must appear in writing so you’ll never be caught off guard.

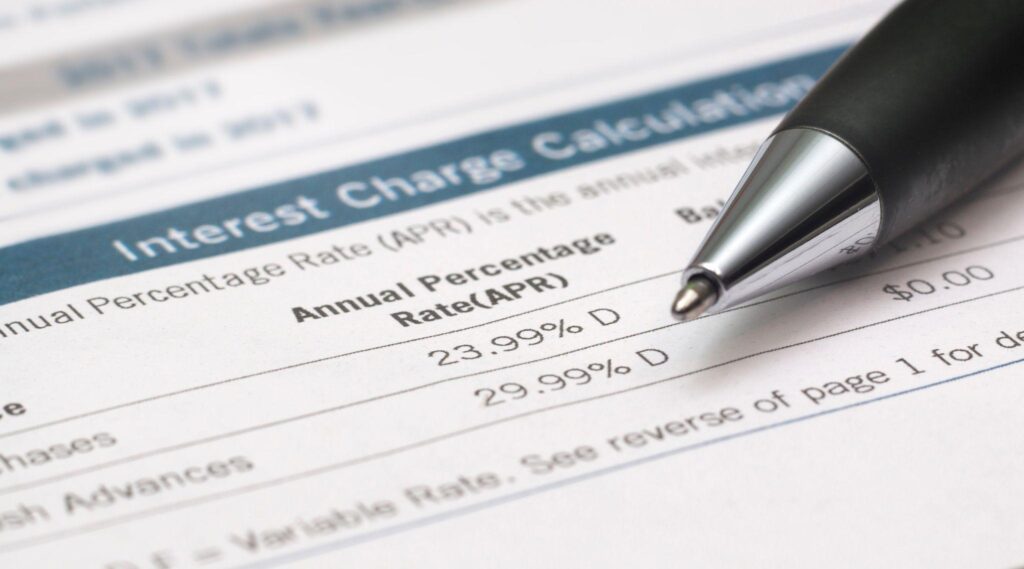

2. The Annual Percentage Rate (APR)

Even for short‑term payday loans, lenders have a legal obligation to list the APR, which reflects the annualized cost of borrowing, including interest and all fees combined. This standardized rate lets you compare different lenders fairly and evaluate how expensive the loan actually is over time. A trustworthy lender will make sure you understand how the APR works and how it affects the total cost of borrowing.

3. Repayment terms and due date

Your payday lender must outline your exact repayment schedule, due date, and payment method. Typically, repayment occurs on your next payday via automatic withdrawal from your checking account. Knowing the date and repayment method in advance helps you plan your budget and avoid missed payments or overdraft fees.

4. Consequences for missed or late payments

If you miss or delay a payment, the lender must disclose what happens before you finalize the loan. This includes any late payment penalties, returned‑check fees, or potential collection actions. Understanding these consequences in advance allows you to maintain control of your finances and avoid costly surprises.

5. Renewal and rollover policies

Some payday lenders allow borrowers to extend their loan term, a process known as a rollover. By law, lenders must disclose whether this option exists, how it works, and any additional costs.

For instance, a rollover may extend your due date but add new fees or interest. Reviewing this information helps you decide whether loan renewal is truly beneficial or too expensive long‑term.

6. Borrower rights and contact information

Every payday loan borrower has a right to clear communication. Lenders must supply current business contact information, including a phone number, address, and email for customer support.

They must also provide details about how to file a complaint with regulatory agencies such as your state’s financial services authority or the Consumer Financial Protection Bureau (CFPB).

These disclosures exist to protect you. By reviewing every detail, you ensure you’re borrowing under fair, transparent conditions. It’s a simple yet powerful step toward safer, more informed financial decisions.

Step-by-step process of how borrower disclosures work

Here’s what typically happens during the payday loan application and approval process, and where your borrower rights fit in:

Step 1: Application submission

You complete an online or in-person application with basic details such as your income, identification, and banking information.

Your right: The payday lender must use this information securely and explain how your data will be stored and used.

Step 2: Loan offer and disclosure review

Once approved, your lender provides a disclosure document that summarizes the loan terms.

Your right: You have the right to review every term, including the APR, fees, and due date, before agreeing. You also request clarification on any confusing points.

Step 3: Loan agreement and funding

After you accept the offer, the lender deposits funds into your bank account (often the same day).

Your right: You’re entitled to a copy of the loan agreement, either printed or digital.

Step 4: Repayment and recourse

You repay the loan on the agreed date, usually through an automatic bank draft.

Your right: If an error occurs or you believe a payday lender misrepresented terms, you have the right to file a complaint with the Consumer Financial Protection Bureau (CFPB) or your state’s financial regulatory agency.

Why knowing your rights matters

Knowing your rights as a payday loan borrower helps you protect your finances, avoid scams, and ensure fairness in your lending experience.

Here’s why it matters:

- Transparency builds trust: A legitimate payday lender will always provide written details before you sign.

- Eliminates confusion: Understanding APR, fees, and payment schedules prevents costly misunderstandings.

- Empowers you to compare: Knowing standard disclosures helps you compare lenders side-by-side and pick the best terms.

- Guards against predatory lending: Awareness discourages lenders from hiding fees or using deceptive marketing.

- Encourages responsible borrowing: When you know the total loan cost, you decide if borrowing fits your budget.

Your rights exist to protect you. When lenders follow the law and borrowers understand it, the payday lending process becomes safer and more transparent for everyone.

Common mistakes borrowers should avoid

While payday loans provide quick relief during financial emergencies, even small misunderstandings lead to unnecessary stress or added costs if you’re not careful.

The best way to use payday loans responsibly is to approach the process with awareness, patience, and an understanding of your rights.

To protect your finances and maintain control, avoid these common mistakes.

1. Skipping the disclosure review

Never sign or accept funds before reading the full disclosure form. Every legitimate payday lender is legally required to outline all fees, terms, and repayment amounts in writing before you commit.

Taking a few minutes to review these details helps you catch hidden fees or unclear language that could become costly later. Responsible borrowers always confirm they understand what they’re signing. Clarity today prevents confusion tomorrow.

2. Ignoring the APR

The annual percentage rate (APR) reflects the real cost of borrowing, including interest and fees. Some borrowers focus only on the loan amount or flat fee, assuming that’s the full expense. But comparing APRs between lenders gives you a clear, side‑by‑side look at which offer is truly more affordable.

Understanding the APR also helps you make smarter decisions going forward. If one payday lender shows a much higher APR than another, consider whether the speed of approval is worth the extra cost. Transparency in APR ensures you’re paying a fair price for short‑term financial help.

3. Assuming all lenders are legitimate

Unfortunately, not every payday loan company operates legally. Unlicensed or predatory lenders often target borrowers in urgent situations, hiding behind attractive marketing or “guaranteed approval” promises. Always verify your lender’s registration in your state before submitting personal information or making a payment.

You check the lender’s status through your state’s Department of Financial Institutions or the Consumer Financial Protection Bureau (CFPB). Working only with licensed, verified lenders protects your rights and ensures your loan terms comply with consumer protection laws.

4. Over‑borrowing

It’s tempting to borrow more than you need, especially when facing multiple expenses. However, payday loans work best for short‑term use; they bridge the gap between paychecks. They aren’t supposed to fund ongoing costs. Borrowing only what you comfortably repay with your next paycheck helps you avoid rollovers, extension fees, or mounting debt.

Before applying, calculate exactly how much you need to cover your immediate expenses. Borrowing within your means keeps repayment manageable and helps you maintain budget balance even after the loan is paid off.

5. Failing to keep records

Many borrowers forget to save paperwork or digital copies after finalizing the loan, but keeping accurate records is essential. Always store your loan contract, payment receipts, and communication history with your lender. These documents protect you if disputes arise, such as incorrect charges or early withdrawals.

If you’re borrowing online, download and save email confirmations, digital agreements, and payment receipts to your personal folder. A responsible payday loan borrower treats documentation as an important tool for maintaining financial control.

Key industry statistics

- Approximately 12 million Americans use payday loans annually

- Many payday loan borrowers access loans online

- Many borrowers don’t read full disclosure documents

Recommended resources and tools

Staying informed is one of the smartest things you can do as a payday loan borrower. When you understand your rights, compare lenders, and track your finances, you’ll reduce risk and strengthen your financial decision‑making. The following tools and resources help you borrow safely, confidently, and responsibly:

1. Consumer Financial Protection Bureau (CFPB)

The CFPB is a federal agency dedicated to protecting consumers in the financial marketplace. Its website provides trustworthy information on loan laws, borrower rights, and complaint procedures.

If you ever feel a payday lender has violated your rights, you submit a formal complaint directly through the CFPB’s online portal. The site also offers helpful guides explaining what responsible lending looks like and what to avoid.

Visit: www.consumerfinance.gov

2. Your State’s Department of Financial Institutions (DFI)

Every state regulates payday loans differently, setting specific rules for licensing, maximum interest rates, and rollover limits. Your state’s financial institutions department helps you confirm whether a lender is legally authorized to operate where you live. Verifying a lender’s license is one of the easiest ways to protect yourself from scams or predatory practices.

Before applying, search your state’s DFI website to:

- Check if the lender is registered and compliant

- Review any prior consumer complaints

- Learn your rights under local lending laws

Pro Tip: Utah borrowers confirm licensing through the Utah Department of Financial Institutions (DFI) website before applying with any payday lender.

3. Loan comparison calculators

Before accepting a loan offer, use a loan comparison calculator to estimate the total cost of borrowing. These online tools break down fees, interest, and the repayment schedule so you see how much your short‑term loan will really cost.

Comparing options side by side helps you identify which lender offers the most favorable terms and ensures you understand the full financial picture before committing.

Pro Tip: A small difference in fees significantly affects the total cost of a loan, especially for short‑term borrowing. Always compare APRs.

4. Budgeting and financial management apps

Budgeting apps like Mint, YNAB (You Need A Budget), or Rocket Money can be powerful allies for tracking income and repayment schedules. They help you stay on top of due dates, monitor spending, and set aside enough funds to repay your loan on time. Using digital tools also reduces the risk of overdrafts or missed payments, which trigger additional fees.

Tip: Sync your budgeting app to send alerts a few days before your payday loan repayment is due.

FAQ

Q: What disclosures must a payday lender provide?

A payday lender must clearly disclose loan amounts, fees, APR, repayment dates, and penalties for missed payments.

Q: Are payday loans regulated?

Yes. Both state and federal laws regulate payday lenders to protect borrowers from unfair terms or hidden costs.

Q: What should I do if my lender didn’t provide disclosures?

Contact your state’s financial regulator or the CFPB immediately. Lack of disclosure violates lending laws and could make the loan terms unenforceable.

Ready to borrow from a lender you trust? USA Cash Services is here.

At USA Cash Services, we believe every payday loan borrower deserves honesty, transparency, and peace of mind. That’s why we strictly follow all state and federal lending laws. We clearly disclose every fee, term, and repayment detail before you sign. There are no surprises or costs. We provide straightforward financial support when you need it most.

Whether you’re facing an emergency expense or a short-term cash gap, we’ll help you navigate the process safely and confidently. Apply today and see why USA Cash Services is trusted by thousands of borrowers who value clear communication, fast funding, and complete transparency.